Arnold DiLaura, Managing Director, AUA Capital Management

December 2014

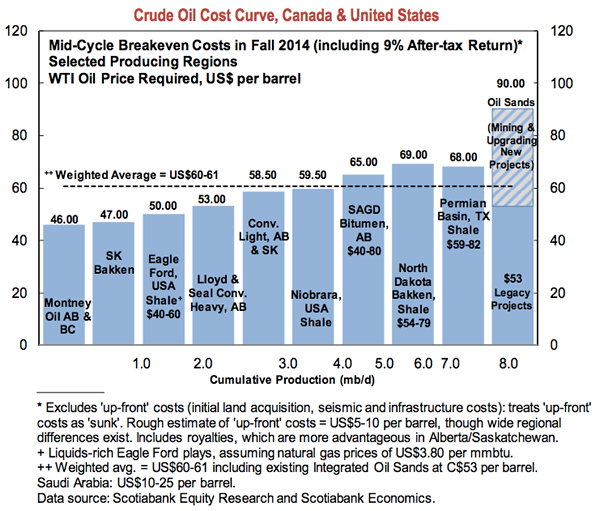

We have found some interesting charts regarding the outlook for oil as we head into 2015. The first is from Scotiabank, and shows the break-even price for various US and Canadian oil fields. They range from over $80 to the mid-40s. Crude is currently trading between $55-60 a barrel.

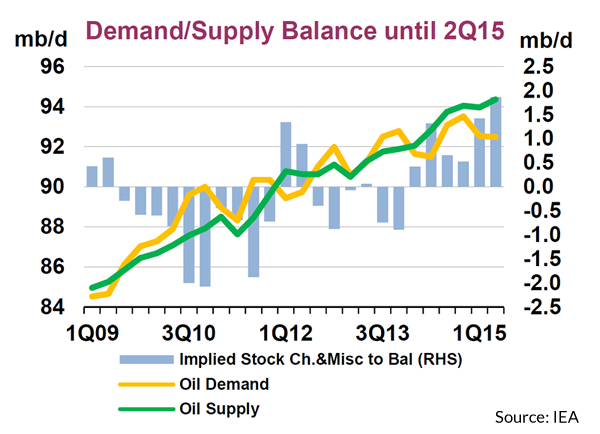

The second chart below is from the IEA and shows a time-series of world production and demand for oil from 2009 projected through 2015. We currently have a 2 million b/d over-supply which is contributing to the price weakness.

The implication of the two charts is that if the Saudis want to take 2-3 million b/d of production capacity out of the market, oil should stabilize at a price in the mid-50’s. There is however, an additional geopolitical factor to consider: One of Saudi Arabia’s arch enemies, Iran, and a key adversary, Russia, both depend on high oil prices to fund their governments and activities which are antithetical to Saudi (and other Gulf Arabs’) interests. If the Saudis (and their allies) were to continue to drive the price of oil down, they would further reduce marginal production capacity worldwide. However, this capacity would not be Iranian or Russian, as they have an imperative to produce almost no matter what the price. The goal would be to curtail funding for the governments that engage in acts (e.g., support for Assad in Syria) which the Saudi’s oppose.

In any event, we had originally thought that prices would need to go lower (between $40-50/barrel) to shake out the higher price producers. Clearly prices could go that low, but if the implications of these charts are correct, then the floor might be at current levels in the mid-50s. If so, we could expect oil to trade in the $50-60 range over the next 6 months to one year.

AUA Capital Management, LLC does not render legal, accounting, or tax advice. This analysis has been prepared solely for informational purposes and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any performance data quoted represents past performance. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Past performance is no guarantee of future results. This data is gathered from what is believed to be reliable sources, but we cannot guarantee its accuracy.

AUA Capital Management, LLC blog, white papers and website are made available for information and educational purposes only. The blog, white papers and website give general information and do not provide investment advice. By reading our blog, white papers and website, you understand that there is no advisor-client relationship created between you and AUA Capital Management, LLC. Although the information on our blog, white papers and website is intended to be current and accurate, the information presented may not reflect the most current developments, regulatory actions or investment decisions. These materials may be changed, improved, or updated without notice. AUA Capital Management, LLC is not responsible for any errors or omissions in the content of the blog, white papers or website or for damages arising from the use or performance of the blog, white papers and website under any circumstances. We encourage you to contact us or other investment advisors for specific investment advice as to your particular matter.

You may print a copy of any part of this blog or white paper for your own personal, noncommercial use, but you may not copy any part of the blog or white paper for any other purposes, and you may not modify any part of the blog or white paper. Inclusion of any part of the content of this blog, white paper or website in another work, whether in printed or electronic, or other form, or inclusion of any part hereof in another web site by linking, framing, or otherwise without the express permission of AUA Capital Management, LLC is prohibited.