Arnold DiLaura, Managing Director

April 2015

Writing covered calls on equity positions in a portfolio is a useful way of generating additional income as the call writer is monetizing a portion of the stock’s potential upside over the option’s 30- or 60-day lifetime.

The risk of covered calls is that at expiry the stock will be higher than the strike price and either the stock will be called away, the short call will have to be bought back, or the option position will be “rolled”– the short call will be bought back and the purchase will be financed by selling a longer-dated, higher-strike price call. Rolling in effect gives the stock further room to appreciate. If a stock is called away, another potential strategy is the use of a cash-secured put which we discuss in more detail below.

When looking at a portfolio, there are two ways to write calls: 1) The first is on a portion of some or all of the individual stocks in the underlying portfolio, 2) The second is to write index call options on the portfolio as a whole. Each technique has its own advantages and disadvantages.

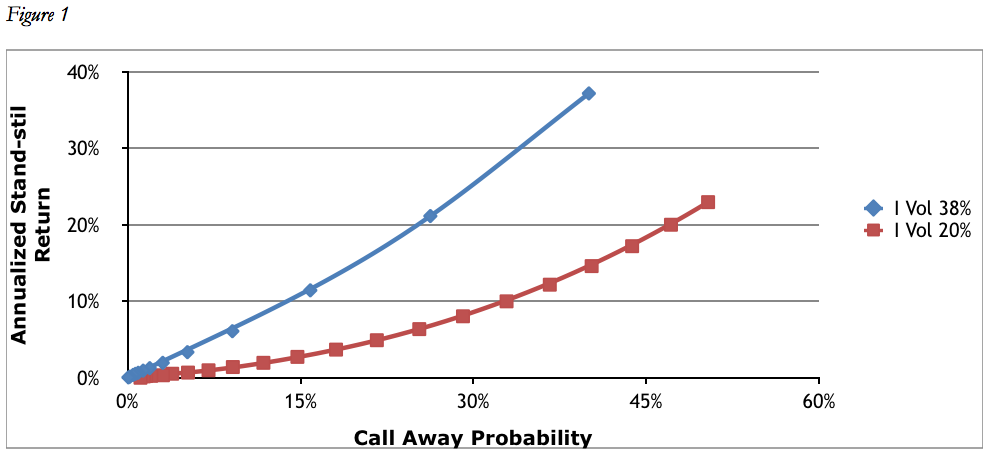

Writing calls on the individual stocks will generate more income, all else being equal. This is because the implied volatility of options on individual stocks is almost always higher than the implied volatility on an index which includes the underlying stocks. All else being equal, the higher the implied volatility, the higher the option premium. Figure 1 below shows a comparison of the annualized stand-still returns at various call-away probabilities for an ETF which trades at a 20% implied volatility versus a 38% implied volatility.

Even though writing calls on the index generates less income, it has certain advantages: 1) The first is simplicity, in that the call writer is writing options on one index, not 30 or 40 stocks, 2) The other advantage is that the individual stocks are free to appreciate unencumbered. If one of the stocks in the portfolio is the subject of a takeover and doubles overnight, the stockholder gets the full gain. If options had been written on the stock, the stockholder would only get the gains up to the strike price.

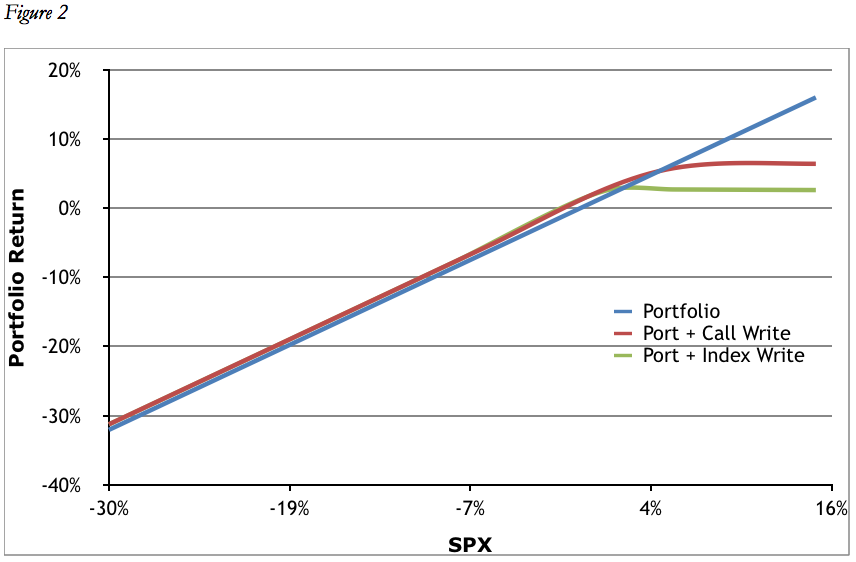

Figure 2 shows a graphic comparison between writing calls on individual stocks in an illustrative large-cap portfolio, and writing an index call on the same portfolio. In this example, the portfolio is equal capital weighted. In selecting options for individual stocks, one can first calculate the probability that any particular strike price will be in- or out-of-the-money at expiry. One can then look for those options that have a 25% probability or less of being in-the-money (ITM), and that still generate a sufficient annualized return. The specific stocks, option strike prices, premiums, percentages out-of-the-money (OTM), and stand-still returns are shown in Table 1. Writing a call on each stock will generate about 80 b.p. in premium (relative to the total value of the equity portfolio) over the 60 day period, or an approximate 4.8% annualized return. Table 1 shows that the option strike prices vary from about 3.5% to over 9% OTM. This means that the stocks can appreciate from 3.5% to 9% over a 60 day period without the risk of being called away.

For comparison purposes we selected and sized an index option on the portfolio as a whole which would generate the same amount of option premium, 80 b.p. As Figure 2 shows, the index strike price is much closer to at-the-money (ATM) than any of the single stocks – about 2%. This means that the risk of underperformance in a rising market is significantly higher with the index option methodology than the single stock option methodology – 2% vs. 5%.

Table 1

| Ticker | Last | Strike | %OTM | Stand-still Return (Annualized) |

| EMC | 26.28 | 28 | 6.54% | 3.31% |

| SNY | 52.56 | 55 | 4.64% | 5.99% |

| CAH | 66.2 | 70 | 5.74% | 3.85% |

| AAPL | 604.71 | 640 | 5.84% | 6.00% |

| NOV | 82.07 | 85 | 3.57% | 6.18% |

| ORCL | 41.56 | 45 | 8.28% | 3.46% |

| MSFT | 39.68 | 42 | 5.85% | 3.63% |

| USB | 41.11 | 43 | 4.60% | 3.28% |

| ECL | 106.67 | 110 | 3.12% | 5.20% |

| TMO | 114.47 | 120 | 4.83% | 8.12% |

| XLK | 36.71 | 39 | 6.24% | 0.74% |

| TWX | 68.8925 | 75 | 8.87% | 3.00% |

| JCI | 46.68 | 50 | 7.11% | 5.14% |

| COP | 77.85 | 80 | 2.76% | 6.20% |

| CELG | 147.65 | 160 | 8.36% | 8.07% |

| MON | 115.9 | 120 | 3.54% | 9.01% |

| GOOGL | 540.39 | 560 | 3.63% | 12.60% |

| PFE | 29.25 | 31 | 5.98% | 5.33% |

| STJ | 64.13 | 70 | 9.15% | 6.08% |

| SPY | 187.55 | 195 | 3.97% | 1.23% |

| WFC | 48.96 | 52.5 | 7.23% | 1.84% |

| QCOM | 79.86 | 85 | 6.44% | 1.62% |

| BA | 129.58 | 135 | 4.18% | 6.76% |

| JNJ | 100.25 | 105 | 4.74% | 1.83% |

| PEP | 85.65 | 90 | 5.08% | 2.38% |

| XOM | 100.67 | 105 | 4.30% | 3.40% |

| WAG | 68.88 | 75 | 8.89% | 6.45% |

| BBT | 37.09 | 39 | 5.15% | 4.37% |

| UTX | 113.1 | 120 | 6.10% | 2.31% |

| DIS | 81.09 | 85 | 4.82% | 6.33% |

| PG | 80.23 | 85 | 5.95% | 1.12% |

| EWBC | 32.95 | 35 | 6.22% | 9.10% |

What about Puts?

Until now we have been talking about using covered calls to generate income on an equity portfolio. Put options, which convey the right to sell a particular stock at a particular price at some point in the future can also be used as part of an options overlay strategy.

One way they can be used is for protection: one can use a portion of the cash premium generated by selling covered calls on individual stocks to purchase broad-based ETF or Index puts (or put-spreads) thus providing a degree of downside protection for the portfolio as a whole.

The second use of puts in an overlay strategy consists of selling cash-secured, out-of-the-money (OTM) puts as a way of potentially acquiring a stock cheaper than its current price. For example, let’s say we like XYZ stock at its current price of $50, but we would like it even more if we could get it for $45. We could sell a 60-day, $45 strike put for $1. If the stock declined to $45 or below at expiry, we would then be obliged to buy the stock at $45. But we would have still taken in the original $1 credit, which is a stand-still annualized return of 13%.

This strategy can also be used for stocks which have been called away. For example, if one wrote an 80 strike call on a stock that had been trading in the 70s but which subsequently shot up over 80, that stock would be called away. However, after the stock was called away one would have $80 in cash, and assuming one still liked the stock, they could write an 80, or even 75, strike put, taking in an additional cash premium while waiting for the stock to decline to where they would buy it again.

Overlay Timing

When are the best times to implement options overlays?

- Anytime an investor or portfolio manager needs to generate more cash than will be provided by the regular interest and dividends from portfolio assets. Selling covered calls can avoid the need to liquidate assets to cover disbursements.

- When equity valuations are stretched and consequently huge gains going forward are less likely. In this environment, where long term equity returns are projected to be in the low single digits, a covered call program could double or triple those returns.

AUA Capital Management, LLC does not render legal, accounting, or tax advice. This analysis has been prepared solely for informational purposes and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. Any performance data quoted represents past performance. Investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Past performance is no guarantee of future results. This data is gathered from what is believed to be reliable sources, but we cannot guarantee its accuracy.

AUA Capital Management, LLC blog, white papers and website are made available for information and educational purposes only. The blog, white papers and website give general information and do not provide investment advice. By reading our blog, white papers and website, you understand that there is no advisor-client relationship created between you and AUA Capital Management, LLC. Although the information on our blog, white papers and website is intended to be current and accurate, the information presented may not reflect the most current developments, regulatory actions or investment decisions. These materials may be changed, improved, or updated without notice. AUA Capital Management, LLC is not responsible for any errors or omissions in the content of the blog, white papers or website or for damages arising from the use or performance of the blog, white papers and website under any circumstances. We encourage you to contact us or other investment advisors for specific investment advice as to your particular matter.

You may print a copy of any part of this blog or white paper for your own personal, noncommercial use, but you may not copy any part of the blog or white paper for any other purposes, and you may not modify any part of the blog or white paper. Inclusion of any part of the content of this blog, white paper or website in another work, whether in printed or electronic, or other form, or inclusion of any part hereof in another web site by linking, framing, or otherwise without the express permission of AUA Capital Management, LLC is prohibited.